I’m currently covering 50 or so publicly traded precious metals companies, and keeping an eye on dozens more.

Part of the juggling act in this market comes down to evaluating these companies for the future based on where gold is now and where it’s likely to be in one, five or 10+ years.

The most responsible method is to base my valuations on a lagging gold price. In my paid content, these days you’ll see me come up with valuations based on $3,500/oz gold.

That’s not because I think gold is likely to dip down to that price – it’s just one more way for me to give my readers and myself a margin of safety in my analysis.

Like in any business, no gold mine plan ever goes off perfectly without a hitch. There’s always some unforeseeable factor that slides the margins around, delays production or raises costs.

Six months ago, I was basing my evaluations on $3,000 gold, or even lower. So for much of the past half year, I’ve been increasing my price targets based on the surge in gold’s price.

These piecemeal target increases also tend to follow earnings reports and company updates that give us a better picture of underlying value of each firm.

“The last time this happened,

we saw 400% gains in only months”

Gold mining is such a tricky business that it’s NEVER an accident when a management team successfully builds a productive mine.

Today, I’ve found a company run by a team that’s already seen a $1.1 billion buyout – back when gold was $1,500/oz.

Today, this same team is doing it all over again, ramping up to first production this January 2026. And with gold at $4,000+, the payout is likely to be much bigger.

But this stock is only selling for ~$500 million equal to $1.14 per share: an 80% discount to $3.03 billion fair value or $7.20 per share.

I’ve released the full details of this gold stock – here for free.

I haven’t been talking much about gold royalty firms lately – and it’s easy to understand why. While gold miners tend to catch every gust and soar when gold is on the move, the royalty firms are much slower moving.

That’s partially because there’s no big single catalyst to move the share price of royalty firms. Even the small ones I cover have a dozen or so projects in various stages of production. If one project starts paying off, it definitely helps the bottom line, but not in the same direct and massive way it would for a small gold miner.

Right now, despite 100%+ average gains across Golden Portfolio (my service dedicated to royalty firms) we’re still seeing a muted response to gold’s historic surge over the past year.

It’s great news for you if you don’t own these firms yet. After this latest gold correction, they’re selling for almost as good of a discount to their gross profit as they were at any time in the past 18 months.

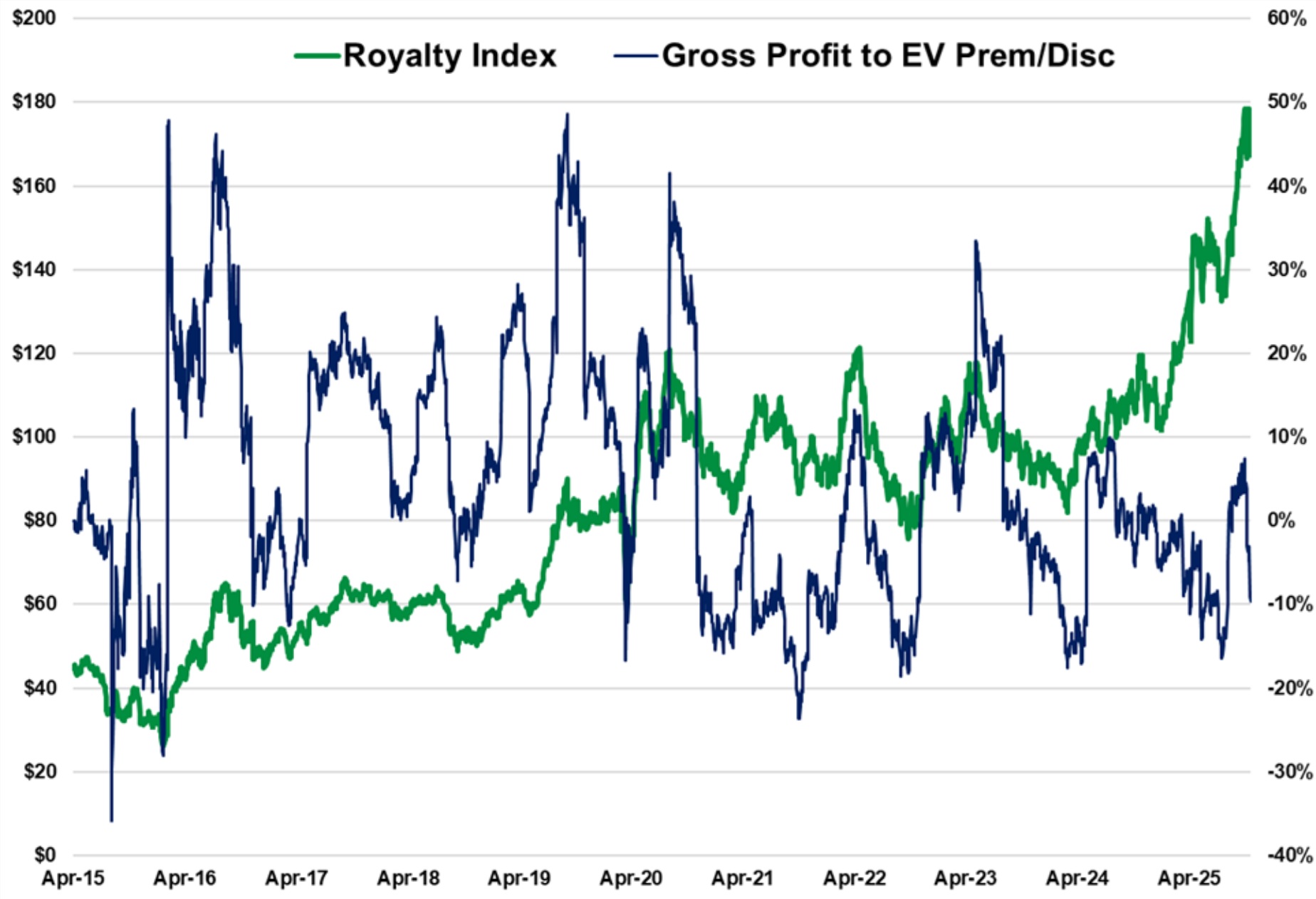

You’ll notice this chart showing the royalty index vs. royalty valuations doesn’t seem to have any rhyme or reason to it. Gold royalty firms just slowly churn higher almost regardless of valuation. But buying royalty firms when they sell at a discount to this valuation has paid off.

And typically this valuation will peak at the end of the bull cycle at ~+30%. We’re still about -10% right now.

If I were to aggressively revalue my gold positions at $4,000/gold, this picture gets even more bullish for the royalty firms. But again: they tend to move so deceptively slow compared to the miners that I worry most people don’t give them a second look.

You’re unlikely to see a daily 10% pop on any gold royalty firm. But you for sure are likely to see a bunch of 1% up days. It’s not as exciting. It’s a slower ride. But I think it’s worth it for the destination.

Best,

Garrett Goggin, CFA, CMT

Lead Analyst and Founder, Golden Portfolio